In addition to asset classes such as equities, ETFs and commodities, investors are increasingly focusing on so-called P2P loans. In recent years, P2P loans have experienced a real boom.

I’ll show you how I would invest $5000 as a newbie in this field with as little risk as possible, which platforms I would use for this and what all there is to consider. I’ll additionally give you an overview of the most important/biggest P2P platforms.

Disclaimer: The information provided here does not constitute investment advice or a recommendation to buy. These are my generally published opinions and experiences as a private investor. I assume no liability for your investment decisions. P2P loans are high-risk products, and no deposit insurance applies. A total loss – however improbable – can never be completely ruled out..

Table of Contents

What are P2P Loans?

A P2P loan, also known as a peer-to-peer loan, is a loan in which both the borrower and the lender are private individuals (hence, “peer-to-peer”). If, on the other hand, the borrowers are entrepreneurs, the term P2B (peer-to-business) loans is used.

As a borrower, you have the advantage that there is no intermediary financial institution, making it less cumbersome and faster for you to get a loan. In particular, banks hardly offer loans in the low four-digit range. Therefore, P2P loans are a good alternative to bank loans.

As a lender, you in turn receive interest on your loaned money and thus participate in a passive income stream. Especially during periods of low interest rates, this is a great way to invest your money. As additional asset classes besides stocks and co. you expand your portfolio and reduce your risk.

What ROI can I expect with P2P Loans?

It is not possible to make a blanket statement about how high your return will be. The rate of return is significantly dependent on the P2P platform, the type of loans and the loan term. In general, higher returns go hand in hand with higher risk.

In 2021, many platforms have reduced their interest rates. Nevertheless, double-digit annual returns are possible. In principle, annual returns of 9-12% are plausible in the current environment. The exception is the Bondora Go and Grow product. There you get an annual return of 6.75%. The lower return is compensated by a higher security. First of all, I am a big fan of Bondora Go and Grow myself.

Overview of the Largest/Most popular P2P Platforms

P2P platforms act as a kind of “middleman” to bring lenders and borrowers together. The following table lists a selection of the largest/best-known platforms:

| P2P Platform | Founding date | Headquarter | Credit Countries | Yield [%] |

| Bondora (Get €5 Bonus)* | 2009 | Estonia | Estonia, Finland, Spain | 6,75 (Bondora Go & Grow) |

| EstateGuru (Get 0,5 % Bonus)* | 2014 | Estonia | Germany, Lithuania, Finland, Latvia, Estonia, Spain | 11.24 (average historical yield) |

| Robocash (Get 0,5% Bonus)* | 2017 | Croatia | Kazakhstan, Spain, Singapore, Vietnam, Philippines | up to 13.3 (if participating in bonus programs, otherwise lower) |

| Mintos | 2015 | Latvia | More than 30 countries | 9.48 (average) |

| TWINO (Get €20 Bonus)* | 2016 | Latvia | Latvia, Poland, Russia, Kazakhstan, Vietnam | 9-11 % (depending on the loan term) |

| PeerBerry | 2017 | Croatia | Lithuania, Poland, Kazakhstan, Ukraine, Russia, Vietnam, Moldova, Sri Lanka, Czech Republic | 10.90 (average) |

How would I Invest €5000 in P2P Loans as a Beginner in 2023?

As a complete beginner in the P2P area, I would first inform myself comprehensively about this asset class. Understanding the investment form is the basic requirement to make wise investment decisions in the long run.

Personally, I would choose three P2P platforms at the beginning, where I would gradually deposit the €5000.

I started with the following three platforms myself:

Why these three P2P Platforms?

All three platforms are user-friendly and are therefore particularly suitable for beginners. On Bondora Go and Grow and RoboCash, most things are automated, presets are hardly necessary. Moreover, Bondora Go and Grow and EstateGuru in particular are relatively low-risk. You can further mitigate risk by investing in different types of loans. While you invest mainly in consumer loans at Bondora and Robocash, you are invested in real estate loans at EstateGuru.

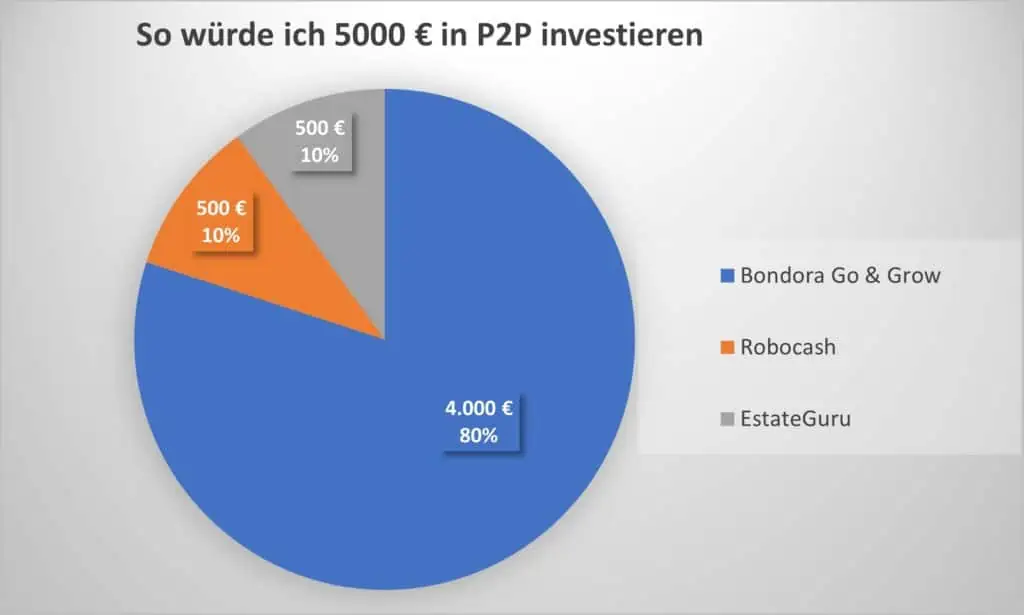

At what proportions would I invest $5000 in the platforms?

I myself allocated $5000 to the three platforms Bondora (Go and Grow), EstateGuru and Robocash at the beginning as follows:

- Bondora Go and Grow: $4000

- Robocash: $500

- EstateGuru: $500

Note: Currently (as of February 2022) you can deposit a maximum of $1000 per month into your Bondora Go and Grow account. It therefore takes a few months before the $4,000 is fully invested.

Bondora Go and Grow

The P2P platform Bondora has been on the market since 2009 and is therefore one of the oldest and most established platforms. On the platform you can invest in different products. In addition to the Portfolio Manager and Portfolio Pro, there is the Bondora Go and Grow* product.

Bondora Go and Grow is a diversified loan portfolio – a large fund, so to speak – consisting of over a hundred thousand individual P2P loans with different rating classes (especially E- and F-rating). Loans are granted in Estonia, Finland and Spain, presumably mainly in the form of consumer loans.

The annual return on Bondora Go and Grow is 6.75%. The actual internal rate of return is higher, but Bondora keeps the surplus as a reserve to compensate for defaults and to minimize risk. Be aware that the return of 6.75% is the maximum return, a lower return is not impossible. However, since Bondora was established, the target return of 6.75% has always been met.

Besides the high level of security compared to most other P2P products, another advantage of Bondora Go and Grow is its instant liquidity. Your capital and the generated interest are not tied up at Bondora Go and Grow and can be cashed out at any time. Therefore, some people call Bondora Go and Grow an alternative to an instant access account. However, this must be expressly contradicted here. There is no deposit insurance with Bondora Go and Grow, unlike instant access accounts. In case of insolvency of the platform, in the worst case all your money would be gone.

Robocash

Robocash has been on the market since 2017 and has therefore been around for a relatively long time. It is important to know that Robocash itself is part of the parent company Robocash Group, which has existed since 2013. RoboCash Group acts as a background lender, while the RoboCash platform offers the loans of the parent company RoboCash. The P2P platform Robocash* is still rather an insider tip, which does not detract from the attractiveness of the platform.

Robocash mainly offers consumer loans. Many loans are short-term (maturity of 7-30 days) and therefore suitable for investors who do not want to tie up their capital for a long time. Loans are currently offered in Kazakhstan, Spain, Singapore, Vietnam and the Philippines. Together with Bondora’s consumer loans (lending countries: Estonia, Finland, Spain), this provides a high level of country diversification.

All loans on Robocash have a repurchase guarantee. If the borrower is 30 days overdue with his payment, you will get the loan back including the interest accrued until then.

The minimum investment amount is €10 per loan and is therefore also well suited for beginners to “get a taste”.

Investing with Robocash takes the form of an automated portfolio builder. After setting some parameters like loan term or interest rate, everything runs automatically, manual investing is not possible.

Robocash as a P2P platform is in my opinion a good way to gain first experience in the P2P environment. The greatest risk probably comes from the insolvency of the parent company Robocash Group. An insolvency of the Robocash platform itself is very unlikely due to the parent company in the background.

EstateGuru

The P2P platform EstateGuru* has been on the market since 2014, which is quite a while in the P2P environment. On EstateGuru real estate loans are made. The advantage of real estate loans compared to consumer loans is the high level of security. Real estate loans are backed by land charges, meaning that the house or land itself is pledged as collateral, making a total default on the loan unlikely. An important parameter at EstateGuru is the LTV (“Loan to Value”). This parameter specifies the ratio of the credit to the deposited value in percent. The lower the LTV, the more collateralized and thus “safer” the investment.

One disadvantage of EstateGuru is the minimum amount per loan. This amounts to €50. So with €500 you could invest in a maximum of 10 different loans. However, this is sufficient for the beginning.

Review of P2P Loans

As a beginner in the P2P sector, it is difficult to keep track of all the different P2P platforms. I myself have ventured into P2P investments with the three platforms Bondora (product Go and Grow), EstateGuru and Robocash and have not regretted it so far.

All three platforms have been reliably paying returns so far, and potential defaults are compensated by buyback guarantees.

I can only recommend starting slowly and gradually building an increasingly diversified P2P portfolio. As another asset class, P2P investments are a nice complement to exchange-traded investments like stocks or ETFs.

Since P2P loans are high risk products, I would limit the share to 10% across all asset classes, but this decision is up to you.

For a detailed guide on taxes and P2P lending, click here.

P2P loans are not the only way to generate passive income. In this post, I’ll introduce you to 36+ methods to build passive income.